Last updated May 13, 2026 with current friendly-fraud rates from Mastercard’s State of Chargebacks report, refreshed Visa VAMP threshold details, and an expanded view on how trust-led decisioning helps merchants tell genuine disputes from coordinated abuse.

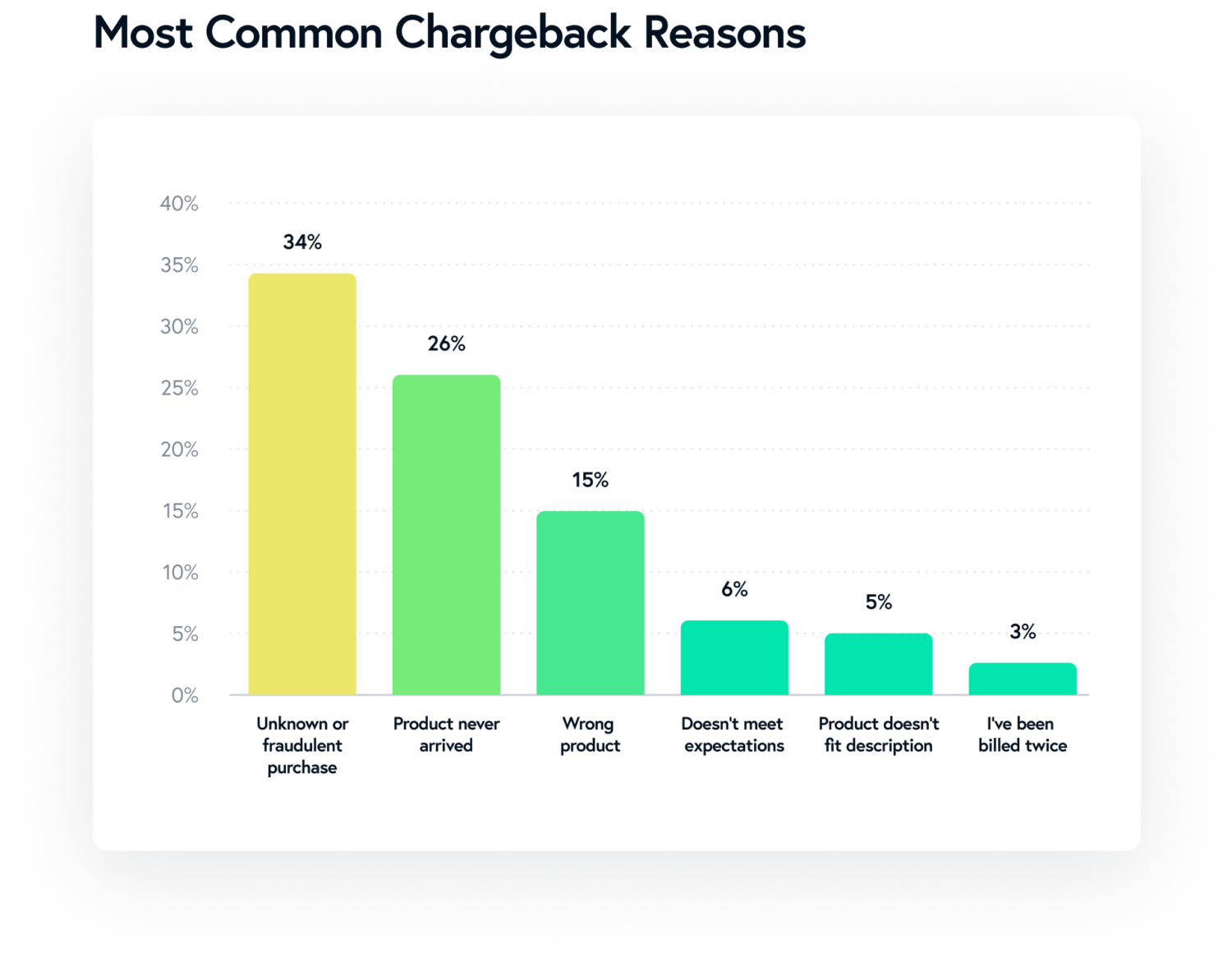

Not every chargeback is a sign of an unhappy customer. A growing share of disputes are first-party (or “friendly”) fraud: the shopper received the product, kept the product, and disputed the charge anyway. Mastercard’s State of Chargebacks 2025 report puts friendly fraud at more than 45% of all chargebacks. Visa estimates friendly fraud accounts for up to 30% of disputes for high-volume online merchants. For many ecommerce categories, it is now the dominant chargeback type.

The economics are unforgiving. Mastercard’s 2025 analysis of the true cost of a chargeback found a single dispute can cost a merchant up to 3.4 times the original transaction value once processor fees, lost goods, operational time, and adjacent penalties are factored in. And new card-network monitoring programs (more on those below) are tightening the thresholds at which excessive chargebacks trigger fees and oversight.

The good news: chargeback fraud usually leaves a pattern. Below are five of the most reliable signs a chargeback is fraud rather than a genuine customer dispute, plus what to do when you spot it.

1. The Customer Initiates a Chargeback Before Attempting a Refund

Some legitimate chargebacks happen because the shopper could not figure out how to ask for a refund. If chargebacks are climbing, walk the customer experience yourself, from first touch to delivery to post-purchase support. Make the refund path crystal clear, with multiple ways to reach your team and prompt responses when shoppers do.

That said, an immediate dispute with no attempt to contact you is a real signal. Look back through customer communications. If the shopper never requested a refund (or was denied and skipped straight to a chargeback), the dispute is more likely first-party fraud than a confused customer. Document what you find. It is exactly the kind of evidence that wins representment cases.

2. The Customer Initiates a Chargeback Before Receiving the Item

When a chargeback lands, confirm the item has actually been delivered. If the dispute was opened before tracking shows delivery (and the shopper never filed an item-not-received claim with you), the chargeback is almost certainly fraudulent.

A related pattern: the actor contacts you directly, pressures you for a refund before the item arrives, and frames the urgency as a way to “save you” the chargeback. Never refund before goods are confirmed delivered. Maintain thorough records for every order: tracking number, delivery photo, signature, anything that proves the package landed where it was supposed to. The brands that win these cases consistently are the ones whose documentation is in order before they need it.

3. The Customer Collects a Refund, Then Initiates a Chargeback (Double Refund)

A double-refund chargeback works like this: the shopper requests a refund, you issue it, and the shopper disputes the charge anyway. Their bank reverses the transaction without realizing you have already returned the money. The shopper walks away with double the refund and the merchant absorbs the loss.

Two practices reduce the exposure. First, issue refunds quickly, because most preemptive disputes happen when the customer thinks you stalled. Second, once a chargeback has been filed, do not issue a refund without coordinating directly with the card issuer or acquiring bank to prevent the duplicate. Treat the documentation around every refund as if you will need to defend it later, because for these cases, you will.

4. The Shopper Ignores Merchant Communications

Customers running first-party fraud usually do not try to resolve the issue with you. They go straight to their bank or card issuer. If the shopper has filed a chargeback and is ignoring your outreach (email, support tickets, phone calls), the dispute is highly likely fraudulent.

Document every contact attempt. Time-stamped outreach showing you tried to resolve the issue directly is some of the strongest representment evidence available, especially under the newer card-network rules that reward merchants for offering a clear pre-dispute resolution path.

5. Multiple Chargebacks From the Same Customer (or Pattern)

Look at the broader transaction history when investigating each dispute. A single shopper filing several chargebacks in a short window, a higher-than-average chargeback ratio on a specific category, or a pattern of disputes tied to the same device, email, address, or payment method is rarely coincidence. It is one actor (sometimes one coordinated group) taking repeated advantage of the system.

This is the place where pattern recognition across the journey pays off. Card-issuer and bank workflows make it easy for a shopper to file a dispute and win, but they were never designed to spot the relationship between three “different” customers using the same shipping address. That work belongs to your risk intelligence layer.

What to Do When You Spot Chargeback Fraud

When the signs above add up to “this is fraud, not a customer dispute,” the response is twofold: defend the case, then prevent the pattern.

Defending the individual case. Build the strongest representment package the card-network rules allow. That generally means proof of delivery, time-stamped customer communications, IP and device records, prior order history, and any signal showing the shopper had previously used and kept the product. Visa’s Compelling Evidence 3.0 rules and Mastercard’s updated dispute frameworks have meaningfully expanded what merchants can submit as evidence, especially around repeat purchases.

Preventing the next one. Repeat first-party fraudsters often come back under slightly different identities. Connecting the patterns (email aliases, address variations, device fingerprints, behavioral fingerprints) and surfacing the link before the next checkout is what keeps the problem from compounding. That is decisioning work, not after-the-fact case review.

Beware of Chargeback Thresholds (The Rules Have Changed)

Chargeback thresholds are the limits payment processors and card networks set on how often a merchant can be disputed before consequences kick in. The rules tightened significantly in 2025.

Visa’s new Acquirer Monitoring Program (VAMP) consolidated five legacy fraud and dispute programs into one. The merchant Excessive threshold launched at a 2.2% combined fraud-and-dispute ratio with a minimum of 1,500 monthly events, with enforcement starting October 1, 2025. The threshold steps down to 1.5% in April 2026. Once a merchant crosses Excessive, Visa imposes an $8 fee per fraud or dispute on top of any acquirer penalties.

Mastercard’s Excessive Chargeback Merchant (ECM) program flags merchants who reach at least 100 chargebacks in a month with a chargeback-to-transaction ratio between 1.5% and 2.99%. Crossing into the ECM tier triggers fees that escalate over time, additional reporting requirements, and, in extreme cases, termination of payment processing services.

The implication for chargeback fraud specifically: friendly fraud counts against these thresholds the same as any other dispute. Letting first-party fraud go undefended is not a neutral cost; it pushes merchants closer to monitoring-program tiers that quietly erode margin.

Read your processor agreement, know your specific thresholds, and watch your chargeback ratio against them. Most acquirers will tell you on request what your current standing is.

How Wyllo Helps Stop Chargeback Fraud Upstream and Win the Disputes Downstream

Repeat chargeback fraudsters create new identities, swap emails and addresses, and look like fresh customers each time. Stopping the pattern requires connecting signals across the full journey, not just at checkout.

Wyllo is the CX-first risk intelligence platform built around exactly this idea. Three pieces of the platform do the most work against chargeback fraud:

- Wyllo Chargeback Management turns representment from a manual scramble into an AI-driven workflow. Disputes are assembled with the evidence each card network actually rewards, win rates climb, and the operational drag of case-building drops sharply. For merchants who qualify, an optional chargeback protection guarantee converts the residual loss into a predictable number.

- Wyllo Payment Fraud Protection stops the highest-risk transactions at the front door using AI screening backed by human fraud experts. Preventing the bad order is always cheaper than defending the dispute.

- Wyllo Claim and Policy Abuse Prevention catches account takeover, claim manipulation, and policy exploitation upstream, before they turn into refunds, chargebacks, or escalations.

The combination is the point. Less reaction. More reason. Designed to think ahead so trusted shoppers keep moving and chargeback abusers keep losing.

Frequently Asked Questions

What is chargeback fraud?

Chargeback fraud (also called first-party fraud or friendly fraud) happens when a shopper disputes a legitimate transaction with their card issuer, often after receiving and keeping the product, with the goal of getting their money back without returning the item. It differs from third-party fraud, where the cardholder’s information is stolen and used by someone else.

How common is friendly fraud in 2026?

Very common. Mastercard’s State of Chargebacks 2025 report found friendly fraud accounts for more than 45% of all chargebacks, and Visa estimates it represents up to 30% of disputes for high-volume online merchants. In some categories it is now the leading chargeback type.

How much does a chargeback cost a merchant?

Mastercard’s 2025 analysis found the true cost of a single chargeback can reach up to 3.4 times the original transaction value once processor fees, lost goods, operational time, and adjacent penalties are factored in. Even a “small” disputed order can produce a multi-hundred-dollar net loss.

What are the warning signs of chargeback fraud?

The most reliable signs appear in clusters: a dispute filed before any refund request, a dispute filed before the item was delivered, a refund followed by a chargeback on the same order (double-refund), the shopper ignoring all merchant outreach, and patterns of multiple chargebacks tied to the same shopper, address, device, or email. Each on its own is suspicious; together they are almost always first-party fraud.

Can a merchant fight back against chargeback fraud?

Yes, through representment. Visa’s Compelling Evidence 3.0 rules and Mastercard’s updated dispute frameworks have expanded what merchants can submit as evidence, particularly around proof of delivery, time-stamped communications, prior order history, and device records. Strong documentation built before disputes arrive is what wins these cases. Many merchants partner with a chargeback management platform to systematize the representment workflow.

What chargeback ratio gets a merchant into trouble?

Both Visa and Mastercard apply network-level monitoring. Visa’s Acquirer Monitoring Program currently sets the merchant Excessive threshold at a 2.2% combined fraud-and-dispute ratio (dropping to 1.5% in April 2026), with $8 fees per fraud or dispute once exceeded. Mastercard’s Excessive Chargeback Merchant program triggers at 1.5% to 2.99% chargeback-to-transaction ratio with at least 100 monthly chargebacks. Most acquirers will tell you your current standing on request.

Bringing It Together

Chargeback fraud is no longer a fringe risk. It is one of the dominant chargeback categories, the network rules are tightening, and the all-in cost per dispute has climbed. The merchants who handle it well treat each chargeback as both a case to defend and a pattern to learn from. Connect the signals across the customer journey, build representment evidence before you need it, and use a partner who can turn the post-purchase mess into a predictable workflow.

Curious how a CX-first risk intelligence approach helps you spot first-party fraud earlier and win more disputes? Wyllo Chargeback Management makes representment painless and predictable, and the broader Wyllo platform stops the patterns upstream before they ever reach your dispute queue.