Last updated May 12, 2026 with current job-market data, refreshed chargeback economics, and an expanded view on the modern risk operations function.

The role of the ecommerce fraud analyst has quietly become one of the most consequential jobs inside a growing online business. Commerce risk has moved beyond the transaction, and the analysts who understand it are no longer just reviewing flagged orders. They are shaping policy, surfacing patterns, and making real-time decisions that protect margin, reduce friction for trusted shoppers, and keep the experience consistent across the customer journey.

Demand is climbing alongside the work. The U.S. Bureau of Labor Statistics projects financial examiner roles to grow 19% from 2024 to 2034, well above the 3% average for all occupations, with roughly 5,700 openings each year. The pressure on the function is climbing too: Juniper Research forecasts global ecommerce fraud losses will reach $48 billion in 2025 and rise to $107 billion by 2029, driven by faster journeys, more automation, and more coordinated abuse patterns.

This playbook lays out what the modern ecommerce fraud analyst does, the skills the best ones bring, and how to think about the build-versus-partner decision when scale outpaces what an internal team can credibly manage.

What Does an Ecommerce Fraud Analyst Do?

An ecommerce fraud analyst monitors transactions and customer behavior to identify fraud, abuse, and policy exploitation, then makes or recommends decisions that protect the business while preserving the experience for trusted shoppers. The role spans four core responsibilities: recognizing shopping patterns, analyzing data and tuning alerts, assessing risk, and investigating incidents.

The most effective analysts work less like gatekeepers and more like decisioning partners. They reduce friction when context says a shopper is trustworthy, add protection when context says they aren’t, and surface the patterns that should reshape policy over time. Less reaction. More reason.

Four Core Responsibilities of an Ecommerce Fraud Analyst

1. Recognize Shopping Patterns and Investigate Anomalies

Analysts establish baselines for customer behavior, transaction history, and account activity. From those baselines, they layer intelligent models and risk detection tooling that flag deviations in real time — unusual geographies, velocities, devices, or behavior patterns that warrant a closer look.

Consider a simple example. An account has six months of consistent purchases inside one geographic region. Suddenly, that same account triggers a series of transactions from a distant location, at unusual hours, with merchandise that doesn’t match its history. A well-tuned system flags the anomaly. The analyst then:

- Confirms the baseline pattern (region, frequency, typical merchant types, spend behavior).

- Reviews the new activity against that baseline (time, geography, merchant, basket).

- Investigates supporting signals (device fingerprint, IP, billing-to-shipping match, account age).

- Confirms whether the behavior is consistent or genuinely anomalous.

- Takes appropriate action: pausing the account, contacting the shopper, escalating, or releasing the order with confidence.

The point is not to block more aggressively. It is to make a confident decision that holds up to scrutiny when the order is good and when it is not.

2. Analyze Data and Tune Automated Alerts

Pattern recognition only scales when the analyst is also a data analyst. The strongest fraud analysts review large transaction datasets to spot trends early, before they become losses. The work usually breaks into a handful of analytical lenses:

- Correlation analysis. Examine the relationships between factors such as transaction types, locations, devices, and customer segments. The connections often hide where individual signals look ordinary on their own.

- Temporal analysis. Watch trends across time. Sudden volume in a particular category during specific hours or days often signals a fresh attack pattern.

- Geospatial analysis. Flag concentrations of activity tied to specific regions or unexpected geographic shifts.

- Chargeback analysis. Review chargeback history for spikes, category clusters, or rate changes that point to either fraud or genuine product or policy issues.

Once the trends are understood, the analyst tunes the alerts that surface real risk without burying the team in noise. A reasonable starting set:

- Unusual purchase amounts well above or below typical order value.

- Rapid succession of orders from a single account or device.

- Shipping and billing mismatches, especially significant address divergence or frequent changes.

- Card and identity mismatches that warrant verification rather than a hard decline.

- High-risk geographies based on the merchant’s specific exposure, not generic blocklists.

- Proxy or VPN signals that suggest the actor is hiding location.

- Off-pattern timing that conflicts with the established baseline.

- Multiple failed payment attempts that may indicate card testing, now affecting roughly a third of global ecommerce merchants according to Mastercard’s research.

- Abnormal device signals — outdated browsers, atypical plugins, unfamiliar fingerprints.

- New accounts with disproportionate first orders.

- Unusual product combinations that may indicate testing or coordinated reseller activity.

- Out-of-character user behavior, including sudden login pattern shifts.

A flag should be a signal that an analyst needs to look more closely, not an automatic decline. The merchants who get this right cross-reference multiple data points before any decision lands on a shopper.

3. Assess Risk and Surface Vulnerabilities

Risk assessment is where the analyst connects internal policy to external reality. The job is to find the gaps the business is silently absorbing and the places where overly strict rules are quietly costing revenue.

The analytical building blocks of a strong risk assessment:

- Historical data. Patterns of past fraud, the methods used, and the policies that did or didn’t catch them.

- Transaction behavior. Typical order value, frequency, payment preferences, and the deviations that genuinely matter.

- Geographic risk. Calibrated to the merchant, not borrowed from a generic regional list.

- Payment method risk. Including how prepaid cards, certain wallets, and emerging payment types behave inside the specific business.

- Device and IP analysis. Unusual hardware or rapid IP changes that warrant context, not blocking by default.

- User account analysis. Account age, login history, and order history evaluated together.

- Velocity checks. Repeated activity inside short windows, especially across the same account, device, or card.

- Chargeback analysis. Seasonal spikes, category clusters, and the gap between gross and net chargeback rates after representment.

- Device fingerprinting. A common identifier across accounts, emails, or sessions that should connect to one actor.

- Machine learning models. Trained on the merchant’s own data, capable of adapting as patterns shift.

- Industry collaboration. Information sharing with peer merchants, processors, and trusted partners about emerging schemes.

- Policy review and refinement. Risk thresholds, verification flows, and exception rules updated on a regular cadence.

The analyst’s most underrated contribution is often telling the business that a rule is too strict. Approving good orders that legacy rules would block is one of the fastest paths to recovered revenue.

4. Investigate Incidents and Manage Disputes

When something does go wrong, the analyst takes the lead on investigation and dispute response. That work spans transaction-level forensics, behavior analysis, and cross-functional coordination with customer support, IT, payment processors, and legal where it applies.

The economics of this phase are unforgiving. Mastercard’s 2025 analysis of the true cost of a chargeback found a single chargeback can cost a merchant up to 3.4 times the disputed transaction value, once processor fees, lost goods, operational time, and adjacent penalties are factored in. The work matters, and so does the speed of the response.

Strong analysts maintain comprehensive documentation, prepare clear case reports, and continuously refine their tactics as fraud techniques evolve. The most useful output of a thorough investigation is rarely the win or loss on a single case. It’s the input back into policy, alert tuning, and the broader risk strategy.

What Makes a Great Ecommerce Fraud Analyst

The job’s hard skills can be taught. The personal qualities are harder to hire for. When evaluating candidates (or developing internal talent), look for:

- Critical thinking. The ability to analyze information dispassionately, weigh competing signals, and reach a confident decision.

- Attention to detail. A pattern is often hiding in a single field that looks correct at a glance.

- Communication skills. Clear writing and the ability to explain complex findings to non-analysts, including customer service, ops, and leadership.

- Empathy. Many flagged orders are good customers. Treating shoppers with respect during verification is part of the brand experience.

- Adaptability. Fraud tactics evolve quickly, and so do legitimate shopper patterns. Comfortable analysts move with that change.

- Time management. A useful day is a triaged one. Priorities shift quickly and decision latency has business cost.

- Problem-solving. Especially the willingness to dig past the obvious explanation when it isn’t quite right.

- Ethical judgment. The role involves sensitive data, real consequences for customers, and ongoing decisions about where to draw lines.

- Resilience. The job has high-pressure moments. Steadiness during them matters.

- Teamwork. Effective analysts work closely with CX, ops, product, payments, and legal. Few important decisions are made alone.

- Curiosity. The best analysts read about emerging schemes, attend industry events, and stay genuinely interested in how the work is changing.

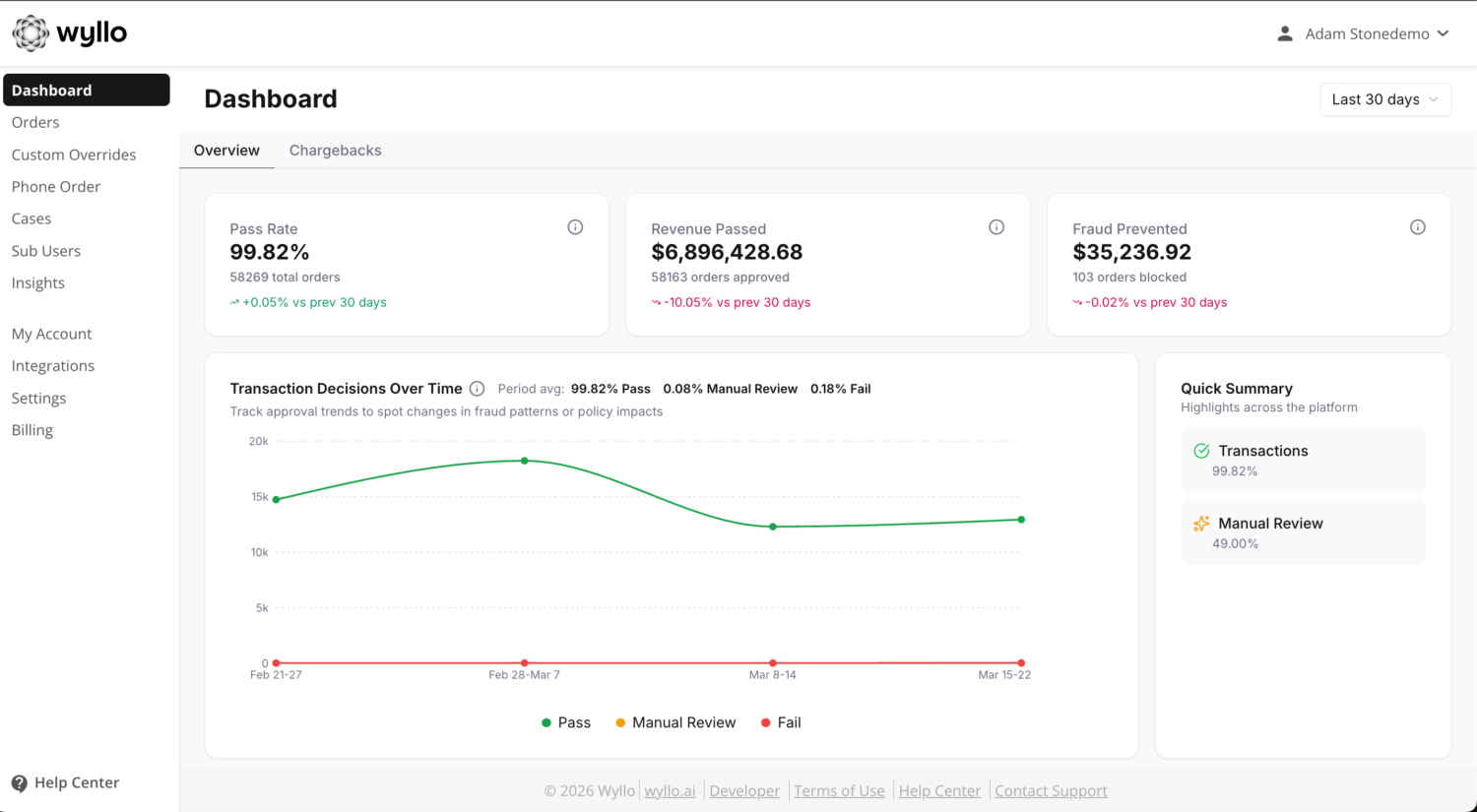

Should You Build an In-House Team or Outsource to a Risk Intelligence Partner?

For some businesses, an in-house analyst team is the right call. For others, especially those scaling fast or operating across many channels and geographies, partnering with a risk intelligence platform that includes analyst expertise tends to be the more economical path.

A few signals that suggest it’s time to consider a partner:

- Growing transaction volume. Volume that consistently outruns the team’s capacity, especially during peak windows.

- Resource constraints. Limited budget, hiring, or tooling capacity to build a credible internal program from scratch.

- Specialized expertise. Risk patterns that require pattern recognition across many merchants, geographies, or categories.

- Fluctuating workload. Sharp seasonal or campaign-driven spikes that make full-time staffing inefficient.

- Cost considerations. The full cost of an in-house program (hiring, training, tooling, retention, coverage) compared honestly to the partner alternative.

- Global operations. Region-specific patterns and payment methods that benefit from a partner with broader exposure.

- 24/7 coverage needs. Round-the-clock review is hard to staff well internally.

- Technology pace. Keeping internal models current with shifting fraud techniques is a serious commitment.

- New markets or product lines. Each expansion exposes the business to unfamiliar patterns and abuse strategies.

- Strategic focus. Internal teams freed to focus on commerce strategy, growth, and customer experience rather than day-to-day case work.

- Regulatory complexity. Industries with heavy compliance overhead benefit from partners who do this work continuously.

- Sustained incident growth. A pattern of rising losses that suggests current controls are not scaling with the business.

The strongest partner relationships replicate the value of a great in-house team, then add the operating depth that comes from seeing patterns across many merchants. Wyllo is the CX-first risk intelligence platform built around exactly this idea: connected signals across the customer journey, merchant-specific context, embedded decisioning in the workflows teams already use, and expert analysts who treat each merchant’s business as their own. Precision over paranoia. Designed to think ahead.

Frequently Asked Questions

What is an ecommerce fraud analyst?

An ecommerce fraud analyst monitors online transactions and customer behavior to identify fraud, abuse, and policy exploitation. The role combines pattern recognition, data analysis, risk assessment, and investigation. The strongest analysts also shape policy, tune detection systems, and partner with CX, operations, and product teams to reduce friction for trusted shoppers while protecting the business from coordinated abuse.

Is fraud analyst a good career?

Yes. The U.S. Bureau of Labor Statistics projects financial examiner roles to grow 19% from 2024 to 2034, much faster than the 3% average for all occupations. As ecommerce volume and fraud sophistication both rise, demand for analysts who can interpret signals across the customer journey continues to climb.

What skills should I hire for in a fraud analyst?

Hire for critical thinking, attention to detail, clear communication, empathy, adaptability, ethical judgment, and curiosity. The technical skills (SQL, analytics platforms, fraud tooling, payments knowledge) can be taught faster than the temperament.

When should an ecommerce business outsource fraud analysts?

Consider partnering with a risk intelligence platform when transaction volume consistently outruns internal capacity, when the business needs 24/7 coverage, when expansion into new markets exposes unfamiliar patterns, when chargeback economics start to compound, or when internal teams would be more valuable focused on growth and customer experience. The right partner brings operating depth across many merchants and embeds decisioning inside the workflows the team already uses.

How much does a chargeback cost a merchant?

Mastercard’s 2025 analysis found the true cost of a single chargeback can reach up to 3.4 times the original transaction value once processor fees, lost goods, operational time, and adjacent penalties are factored in. The dispute fee itself usually runs $20 to $100, with additional bank-handling fees on top.

How is the role of a fraud analyst changing?

The work is shifting from blocking individual transactions to making trust-led decisions across the full customer journey. Modern analysts spend more time on connected context, coordinated abuse detection, and policy refinement, and less time on one-off transaction review. The brands seeing the strongest results treat the function as a risk intelligence team, not a fraud-prevention afterthought.

Bringing It Together

The ecommerce fraud analyst’s role has grown up alongside the customer journey it protects. Connected signals, merchant-specific context, and embedded decisioning have replaced the older model of standalone case review. Whether the work lives inside a growing internal team or alongside a partner who brings broader pattern visibility, the goal is the same: protect margin, reduce unnecessary friction for trusted shoppers, and make confident decisions across the relationship.

Curious how a CX-first risk intelligence approach could complement or replace your in-house fraud function? Wyllo helps commerce teams turn connected context into trust-led decisions across the customer journey.