A Practical Chargeback Prevention Playbook for Risk and Payments Leaders: Screening, Alerts, Evidence, and Post-Purchase Workflows

Chargebacks stopped being a back-office nuisance a while ago. Mastercard’s global chargebacks outlook projects worldwide chargeback volume reaching 337 million by 2026, a 42% climb from 2023. Mastercard’s analysis of the true cost of a dispute puts the real damage at up to 3.4 times the original transaction value once fees, lost goods, and operational time are counted. And the card networks have tightened the thresholds that decide when “a chargeback problem” becomes a compliance problem.

Chargeback prevention, done well, is not one tool or one team. It is a layered discipline that stops disputes before they are filed: screening risky transactions before they settle, intercepting disputes at the pre-dispute stage through alerts, maintaining evidence that wins (and deters) illegitimate claims, and running post-purchase risk workflows that catch abuse before it ever reaches an issuer. In Wyllo’s experience, the merchant programs that treat those four layers as one connected system outperform the ones that bolt on point solutions after the ratio spikes.

This guide walks through each layer in practical terms: what to implement, what to measure, and where the 2026 rule changes reward preparation. It is written for the people who own the number, which is to say risk and payments leaders at online retailers.

Why Chargeback Prevention Is Harder in 2026

Three shifts define the current chargeback prevention landscape.

First-party fraud now drives the majority of dispute pain. Mastercard’s State of Chargebacks research found that first-party (friendly) fraud accounts for more than 45% of all chargebacks, and Visa’s friendly fraud insights estimate it makes up as much as 30% of disputes for high volume online merchants. The Merchant Risk Council’s Global eCommerce Payments and Fraud Report now ranks refund and policy abuse as the top fraud threat in ecommerce, displacing traditional payment fraud for the first time. The dispute your team fights in 2026 is less likely to come from a stolen card and more likely to come from a real customer who kept the product.

The consumer fraud backdrop keeps inflating dispute volume. FTC data released in June 2026 show reported fraud losses hit roughly $16 billion in 2025, the highest on record and up about 25% year over year. Every wave of genuine fraud teaches more consumers that disputing a charge is easy, and some of them start using the dispute button as a refund shortcut.

The thresholds got tighter. Visa consolidated its fraud and dispute monitoring into the Visa Acquirer Monitoring Program (VAMP), and per the Merchant Risk Council’s guidance on the stricter VAMP thresholds, the “excessive” merchant threshold dropped to 1.5% in April 2026 for most regions. Visa’s VAMP fact sheet lays out the mechanics: the ratio combines reported fraud and non-fraud disputes against settled card-not-present transactions, and merchants above the line face enumerated fees per disputed transaction and acquirer scrutiny. A ratio that was survivable in 2024 can put you in a monitoring program in 2026.

The net effect: prevention is no longer just cheaper than fighting disputes. For merchants near the thresholds, it is the only lever that actually works, because a won representment recovers revenue but does not remove the dispute from your ratio.

Where Chargebacks Actually Come From

Effective ecommerce risk management starts by separating chargebacks into their three real sources, because each source responds to a different prevention lever.

Third-party fraud. A stolen card or compromised account produces a transaction the cardholder genuinely never made. The cardholder disputes it, and the issuer sides with them, correctly. The only fix is stopping the transaction up front, which is a screening problem.

First-party (friendly) fraud. The cardholder made the purchase, received the goods, and disputed anyway: sometimes opportunistically, sometimes because a family member ordered, sometimes as deliberate serial abuse. This responds to evidence, pre-dispute resolution, and pattern detection across the customer journey.

Merchant error and confusion. Unrecognizable billing descriptors, slow refunds, unclear subscription terms, missed delivery updates, unreachable support. These disputes are self-inflicted and are the cheapest to eliminate.

Most merchants over-invest in the first category and under-invest in the other two, which is exactly backwards given where the volume has moved. The four layers below cover all three sources.

Layer 1: Transaction Monitoring and Pre-Sale Screening

The first layer of chargeback prevention is deciding well at the moment of purchase. Every fraudulent order you approve is a near-certain future dispute; every good order you decline is lost revenue and a customer who may not return. The goal is not maximum blocking. It is accurate decisioning.

What strong screening looks like in 2026:

- Score intent, not just identity. Device fingerprints, behavioral signals, address and email history, network patterns across merchants. A payment instrument was never a reliable proxy for a person, and the useful question is not only “is this card legitimate” but “what is this buyer actually here to do.”

- Run transaction monitoring continuously, not just at checkout. Velocity spikes, card testing bursts, mismatched geographies, and rapid retries after declines all show up in real time if something is watching. Catching a card testing run early prevents dozens of downstream disputes at once.

- Route the gray zone to review instead of auto-declining it. The orders that are neither clearly good nor clearly bad are where false declines happen. A human-in-the-loop review path protects approval rates while keeping genuinely risky orders out of the settlement file.

- Apply verification proportionately. AVS, CVV, and step-up authentication such as 3-D Secure have real value on high risk orders and real cost on low risk ones. Blanket friction pushes good customers away without meaningfully improving online retail security.

One caution on tooling: fraud prevention tools are frequently graded on how much fraud they block, which quietly rewards over-blocking. Grade yours on the pair of numbers that matters, fraud rate and approval rate together. Payment fraud protection that “wins” by declining more good customers is not winning.

Layer 2: Catch Disputes Early With Chargeback Alerts

Even excellent screening cannot prevent a cardholder from picking up the phone. The second layer intercepts disputes after the transaction but before they become formal chargebacks.

The card networks operate the two rails that matter:

- Ethoca Alerts (Mastercard). When a cardholder contacts a participating issuer, Ethoca notifies the merchant, typically within hours, creating a short window to refund, stop shipment, or resolve directly before the case escalates into a chargeback.

- Verifi and Rapid Dispute Resolution (Visa). Verifi’s alerting works similarly on the Visa side, and Rapid Dispute Resolution (RDR) goes further: merchant-defined rules automatically resolve qualifying pre-disputes inside Visa’s dispute platform, often before your team even sees the case.

Two operating disciplines make alerts pay for themselves:

Decide the refund-versus-fight rule in advance. Alerts cost money per case, so a rule set that auto-resolves low value, low winnability cases and routes high value or suspicious cases to review converts alert spend into predictable savings. An alerted case you resolve is a chargeback fee you never pay, merchandise you may still stop from shipping, and an angry escalation you avoid.

Confirm how each resolution path counts against your ratios. Network monitoring rules have changed several times in two years, and how alert-resolved and auto-resolved cases are tallied under VAMP depends on case type and current network policy. Get the current answer from your acquirer in writing and recheck it when thresholds change. Guessing here is how merchants discover a monitoring program from the inside.

Alerts also generate underused intelligence: they tell you which products, price points, and traffic sources generate disputes fastest. That data belongs in your screening models, not in a monthly PDF nobody reads.

Layer 3: Build Evidence That Wins and Deters

The third layer assumes some disputes will always get through, and makes sure the illegitimate ones lose.

Visa’s Compelling Evidence 3.0 rules changed the economics of fighting friendly fraud. Per Visa’s merchant readiness guidance, a merchant disputing a “fraud” claim can now prevail by showing two prior undisputed transactions from the same cardholder, between 120 and 365 days old, where at least two core data elements match the disputed order, one of which must be the IP address or the device ID. In plain terms: if you keep clean order histories tied to device and IP data, a repeat customer who cries fraud on their fifth order is now a winnable, even blockable, case.

Evidence readiness is a habit, not a scramble:

- Capture at order time, not at dispute time. IP address, device fingerprint, account login, shipping address, and email for every order, stored so they can be joined across a customer’s history in minutes.

- Prove delivery every time. Tracking, delivery confirmation, photo or signature where the economics justify it. Disputes filed before delivery, with no item-not-received claim to you, are among the clearest fraud signals there are.

- Log every customer contact. Time-stamped outreach and support transcripts showing the shopper skipped straight to their bank are some of the strongest representment evidence available, and the newer network rules increasingly reward a documented pre-dispute resolution path.

- Fight selectively and learn from outcomes. Representment win rates improve when you stop fighting everything and start fighting the cases your evidence actually supports. Feed the loss reasons back into layers 1 and 4.

For the behavioral patterns that separate genuine disputes from first-party abuse, our field guide to the five signs a chargeback is actually fraud goes deeper on what to look for and what to do when you find it.

And keep the strategic point in view: evidence wins battles, prevention wins the war. A successful representment recovers the revenue but the dispute already counted toward your thresholds. If the same actor is filing disputes across aliases, winning cases one at a time is treading water. Connecting them and stopping the next order is the fix.

Layer 4: Post-Purchase Risk Workflows for Chargeback Prevention

The fastest growing source of disputes never looks like payment fraud at checkout. It looks like a refund request, an item-not-received claim, a return that comes back wrong, or a support conversation that ends with “I’ll just call my bank.” The fourth layer of chargeback prevention lives here, after the sale.

Screen claims and refund requests with the same seriousness as transactions. An INR claim from an address with three prior INR claims under different names is not a delivery problem. Risk-scoring claims, returns, and refund requests catches abuse in the support channel before it converts into either a policy loss or a chargeback.

Coordinate refunds and disputes to kill double refunds. The double refund pattern (customer collects your refund, then disputes the charge anyway) thrives on disconnected systems. Two rules eliminate most of it: refund promptly when you decide to refund, since stalling provokes preemptive disputes; and once a dispute exists, never refund outside the dispute process itself.

Link repeat actors across identities. Serial abusers rotate emails, addresses, and payment methods, but device, behavioral, and network fingerprints connect them. The issuer’s dispute workflow was never designed to notice that three “different” customers share a shipping address. Your risk layer has to be the place where that pattern becomes a decision.

Make policy a risk instrument. Trusted customers get instant refunds and generous terms; documented abusers get stricter verification, refund-on-return-receipt, or a declined order next time. Dynamic policies protect the experience for the customers who fund the business, which is the actual point of online retail security.

Put risk context in front of support agents. Most friendly fraud passes through a human conversation before it becomes a dispute. An agent who can see order risk signals and a recommended action resolves the moment correctly; an agent flying blind either gives away margin or manufactures the next chargeback.

Tighten the Operational Basics

None of the four layers excuses skipping the unglamorous fixes that erase merchant-error disputes almost for free:

- Billing descriptors a cardholder recognizes. Your legal entity name is not your brand name, and “unrecognized charge” remains a leading avoidable dispute trigger.

- Plain-language policies at the decision moment. Shipping times, return terms, and subscription renewal terms stated where the customer commits, not buried in a footer.

- Proactive order and delivery communication. Confirmation, shipment, tracking, delay notices. Informed customers file fewer “where is my order” disputes.

- Easy cancellation for subscriptions. A customer who cannot find the cancel button finds the dispute button. Make cancellation as findable as checkout and you trade a small churn number for a smaller chargeback number.

- Fast, reachable support. Many disputes are simply the shortcut a customer takes when your queue is slower than their bank’s phone line.

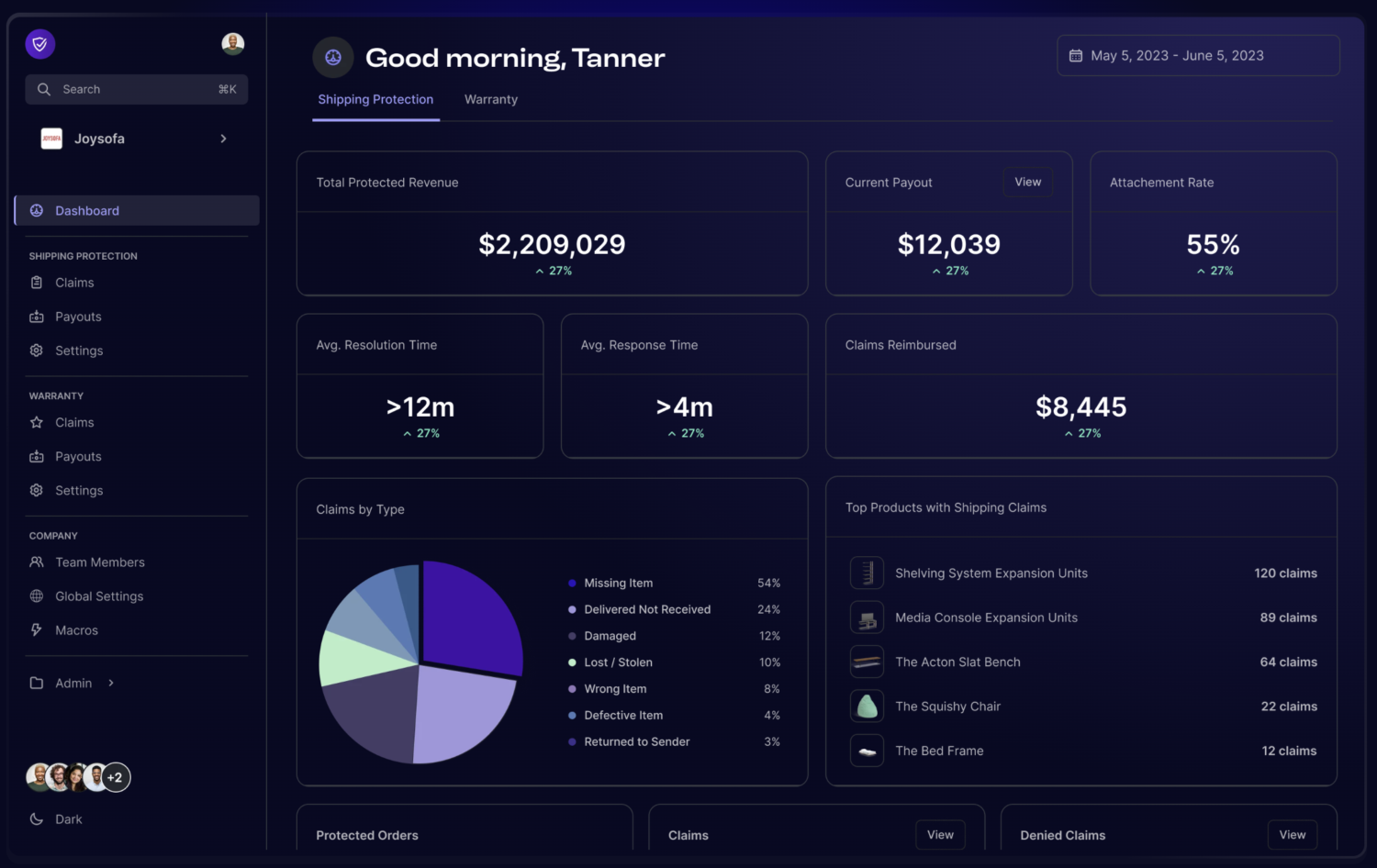

Measure What Moves the Number in Chargeback Prevention

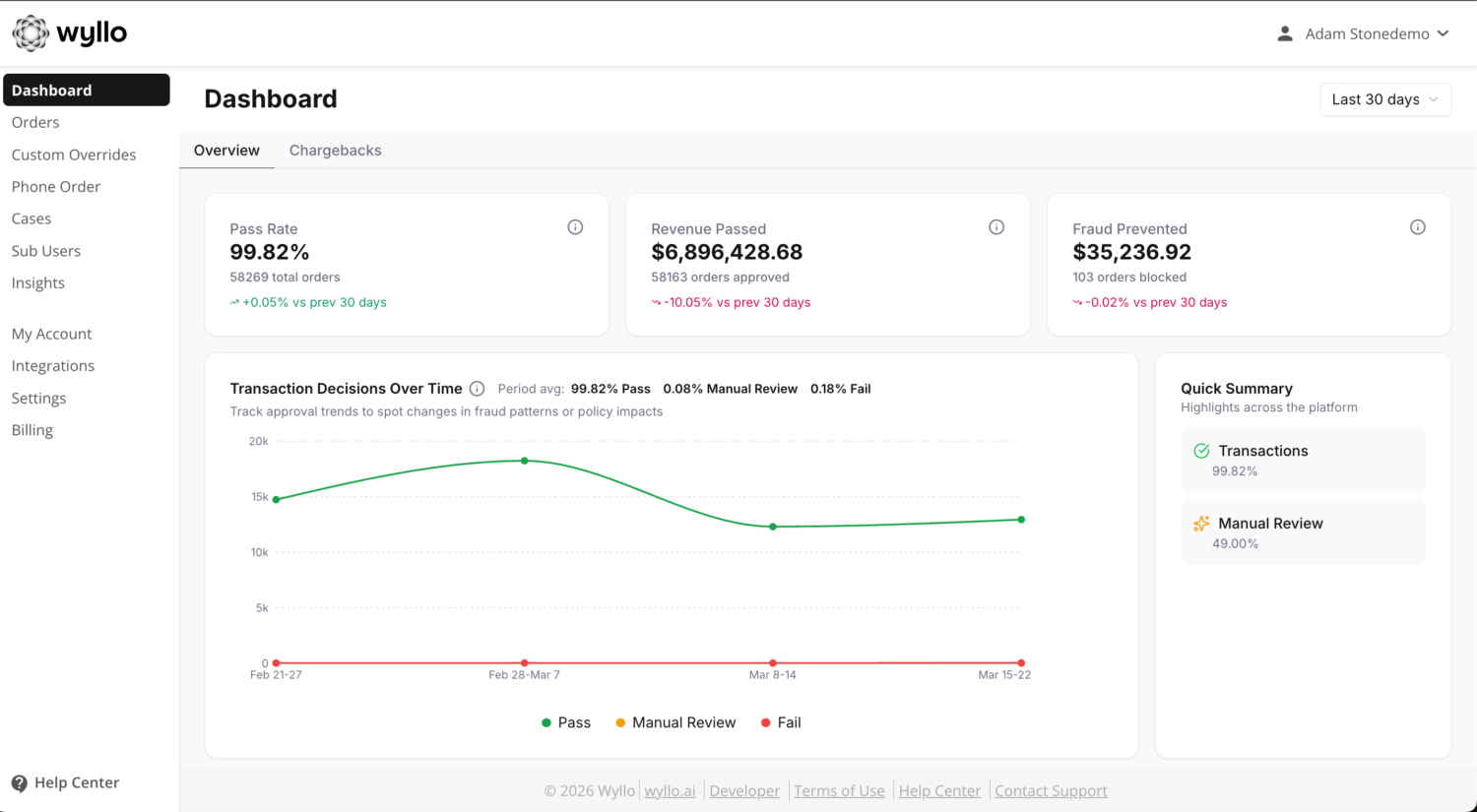

Chargeback prevention is a management system, and it needs instrumentation. The metrics that belong on a risk and payments leader’s dashboard:

- Dispute ratio, computed the network’s way. Track your VAMP-style ratio (fraud plus disputes over settled card-not-present transactions) weekly, with alerting well below the 1.5% excessive line and the earlier warning tiers. Trends matter more than snapshots; thresholds are hit by trajectories.

- Dispute rate by reason code and by source. Third-party fraud, first-party abuse, and merchant error need separate lines, because they have separate owners and separate fixes.

- Alert conversion. Share of alerted cases resolved before becoming chargebacks, and net savings per alert after fees.

- Representment win rate and evidence completeness. Win rate by reason code, plus the percentage of orders with dispute-ready evidence captured at order time.

- False decline rate alongside fraud rate. The pair, always together. Optimizing either alone quietly damages the other.

- Time from dispute to evidence submission. Deadlines are unforgiving, and speed correlates with wins.

Reviewed monthly with owners attached, these numbers turn chargeback management from an inbox into an operating discipline.

How Wyllo Helps with Chargeback Prevention

Everything above works better when the four layers share one brain, because the signal that prevents a chargeback rarely lives in the system where the chargeback lands. That is the design premise of Wyllo, the risk intelligence platform for commerce: intent-aware decisioning across the full customer journey, so the pattern spotted at checkout informs the claim decision, and the dispute outcome sharpens the next screening call.

- Wyllo Payment Fraud Protection screens every transaction with AI plus expert human review, maximizing approvals while stopping the fraud that becomes tomorrow’s disputes.

- Wyllo Chargeback Management handles dispute responses and representment end to end, with chargeback protection for eligible orders.

- Wyllo Claim and Policy Abuse Prevention catches friendly fraud and policy exploitation in the post-purchase window, before it becomes a chargeback.

- Wyllo Return Fraud and Abuse Prevention risk-scores returns and refund claims so serial abuse gets stopped and honest customers keep their easy returns.

- Wyllo CX Support puts risk scores and next-best actions inside your support tools, so agents resolve risky moments instead of escalating them.

Less reaction. More reason.

Frequently Asked Questions

What is chargeback prevention?

Chargeback prevention is the set of practices that stop payment disputes before they are formally filed: screening transactions for fraud before settlement, resolving cardholder complaints at the pre-dispute stage through network alert programs, maintaining evidence that deters and defeats illegitimate disputes, and catching post-purchase abuse (refund, claim, and policy abuse) before it converts into a chargeback. It matters because a disputed transaction counts against network monitoring thresholds even if the merchant later wins the case.

How do chargeback alerts work?

When a cardholder contacts their bank about a charge, participating issuers send a notification through Mastercard’s Ethoca or Visa’s Verifi network before the complaint becomes a formal chargeback. The merchant typically has a short window (often 24 to 72 hours) to refund the transaction, stop fulfillment, or resolve the issue directly. Visa’s Rapid Dispute Resolution goes a step further by auto-resolving qualifying cases according to rules the merchant defines in advance.

What chargeback ratio triggers Visa’s monitoring program in 2026?

Under the Visa Acquirer Monitoring Program (VAMP), the merchant-level “excessive” threshold is a 1.5% ratio of reported fraud plus non-fraud disputes against settled card-not-present transactions in most regions as of April 2026, with a minimum activity floor before a merchant is assessed, according to the Merchant Risk Council’s summary of the current thresholds. Merchants above the line face per-transaction enforcement fees and acquirer remediation pressure. Because network rules continue to evolve, confirm current thresholds and counting rules with your acquirer.

Does winning a chargeback dispute lower my chargeback ratio?

No. A successful representment recovers the transaction revenue, but the dispute itself still counts toward your network monitoring ratios. That is why prevention (screening, alerts, and post-purchase workflows) is the only reliable way to manage threshold exposure, while representment is how you recover losses from the disputes that get through.

What is the difference between chargeback prevention and chargeback management?

Prevention covers everything that keeps a dispute from being filed: accurate fraud screening, pre-dispute alerts, clear descriptors and policies, and post-purchase abuse detection. Chargeback management is the operational discipline around disputes that do occur: responding to alerts, compiling evidence, submitting representments, and feeding outcomes back into prevention. Mature programs run both as one loop rather than two departments.

How do you prevent friendly fraud chargebacks?

Combine deterrence with detection. Deterrence means clean descriptors, documented delivery, logged customer communication, and evidence practices aligned to Visa’s Compelling Evidence 3.0, which lets merchants use a cardholder’s own purchase history to defeat false fraud claims. Detection means risk-scoring refund requests and claims, linking repeat abusers across aliases and payment methods, and giving support agents the risk context to resolve suspicious requests before the customer’s bank does it for them.

Bringing It Together

The merchants with the lowest dispute ratios in 2026 do not have one heroic tool. They have four layers that talk to each other: screening that judges intent at the moment of purchase, alerts that intercept complaints before they harden into chargebacks, evidence that makes illegitimate disputes a losing proposition, and post-purchase workflows that catch abuse where it now actually lives, in returns, claims, and support conversations.

The industry’s direction of travel is clear. First-party abuse keeps growing, network thresholds keep tightening, and the boundary between “fraud problem” and “customer experience problem” keeps dissolving. That favors merchants who treat chargebacks as an intelligence problem spanning the whole customer journey, and it punishes merchants still fighting last decade’s stolen-card war at checkout only.

Curious how intent-aware decisioning would change your dispute ratio and your approval rate at the same time? Start with Wyllo Chargeback Management for the dispute layer, or explore the broader Wyllo platform for connected intelligence across the full customer journey.