A Decision-Stage Guide for Weighing Detection Accuracy, Customer Experience, Scalability, and Post-Purchase Risk in Ecommerce Fraud Protection Software

The stakes of this purchase keep rising. Juniper Research projects ecommerce fraud losses climbing from $56 billion in 2025 to $131 billion by 2030, driven by AI-assisted attacks and escalating friendly fraud. And the losses you see are the smaller half of the bill: LexisNexis Risk Solutions’ True Cost of Fraud study puts the real cost at $4.61 for every $1 of direct fraud in US retail and ecommerce once investigation, recovery, and operational drag are counted.

Choosing ecommerce fraud protection software is harder than it was five years ago for a simple reason: the problem it has to solve got wider. A tool that only scores checkout transactions now addresses a shrinking share of where losses actually happen. At the same time, the cost of over-blocking has never been clearer, because every false decline is revenue handed to a competitor along with the customer attached to it.

This guide gives ecommerce managers and fraud leaders a practical evaluation framework: what the category needs to protect in 2026, the four criteria that separate vendors, what changes for subscription brands, and the questions worth asking before you sign.

What Ecommerce Fraud Protection Software Must Handle in 2026

Ecommerce fraud protection software evaluates orders, accounts, and post-purchase activity to stop fraud and abuse while approving legitimate customers. The operative word is “and”: modern platforms are judged as much on the good orders they approve as on the bad ones they block.

The scope question matters most. The Merchant Risk Council’s Global eCommerce Payments and Fraud Report now ranks refund and policy abuse as the top fraud threat in ecommerce, ahead of traditional payment fraud, with the average merchant facing multiple distinct attack types in a single year. Mastercard’s State of Chargebacks research finds first-party (friendly) fraud driving more than 45% of all chargebacks. The threats that grew fastest live after the purchase: refund and claim abuse, item-not-received scams, promo and account farming, serial returns, and disputes filed by real customers.

So when you evaluate fraud prevention tools, the first sorting question is scope: does this protect the transaction, or the journey? A checkout-only score leaves your returns desk, support team, and chargeback queue to fend for themselves, and that is where the growth in losses is.

Start With Your Risk Profile, Not a Feature List

Vendor comparisons go wrong when they start with feature checklists. Start instead with an honest picture of your own exposure, because the right software for a flash-sale sneaker brand is not the right software for a subscription supplement company.

Four questions define your profile:

- What is your actual fraud mix? Pull twelve months of losses and classify them: stolen-card fraud, friendly fraud chargebacks, refund and claim abuse, promo abuse, account takeover, reseller activity. Weight your evaluation toward where the money went, not where the demos are flashiest.

- What does a false decline cost you? High margin, high repeat-purchase businesses bleed lifetime value with every wrongly declined order. If your economics depend on retention, decision accuracy and review paths matter more than raw blocking power.

- What experience did you promise customers? Generous returns, instant refunds, and low-friction checkout are competitive weapons. The software has to protect those promises for good customers while withdrawing them from abusers, which requires decisioning nuance, not blanket rules.

- Where will you be in three years? New markets, new channels, marketplace expansion, a subscription line. Migrating fraud systems mid-growth is painful, so buy for the roadmap, not the current quarter.

Criterion 1: Detection Accuracy You Can Verify

Every vendor claims accuracy. The evaluation question is whether they will let you verify it on your traffic.

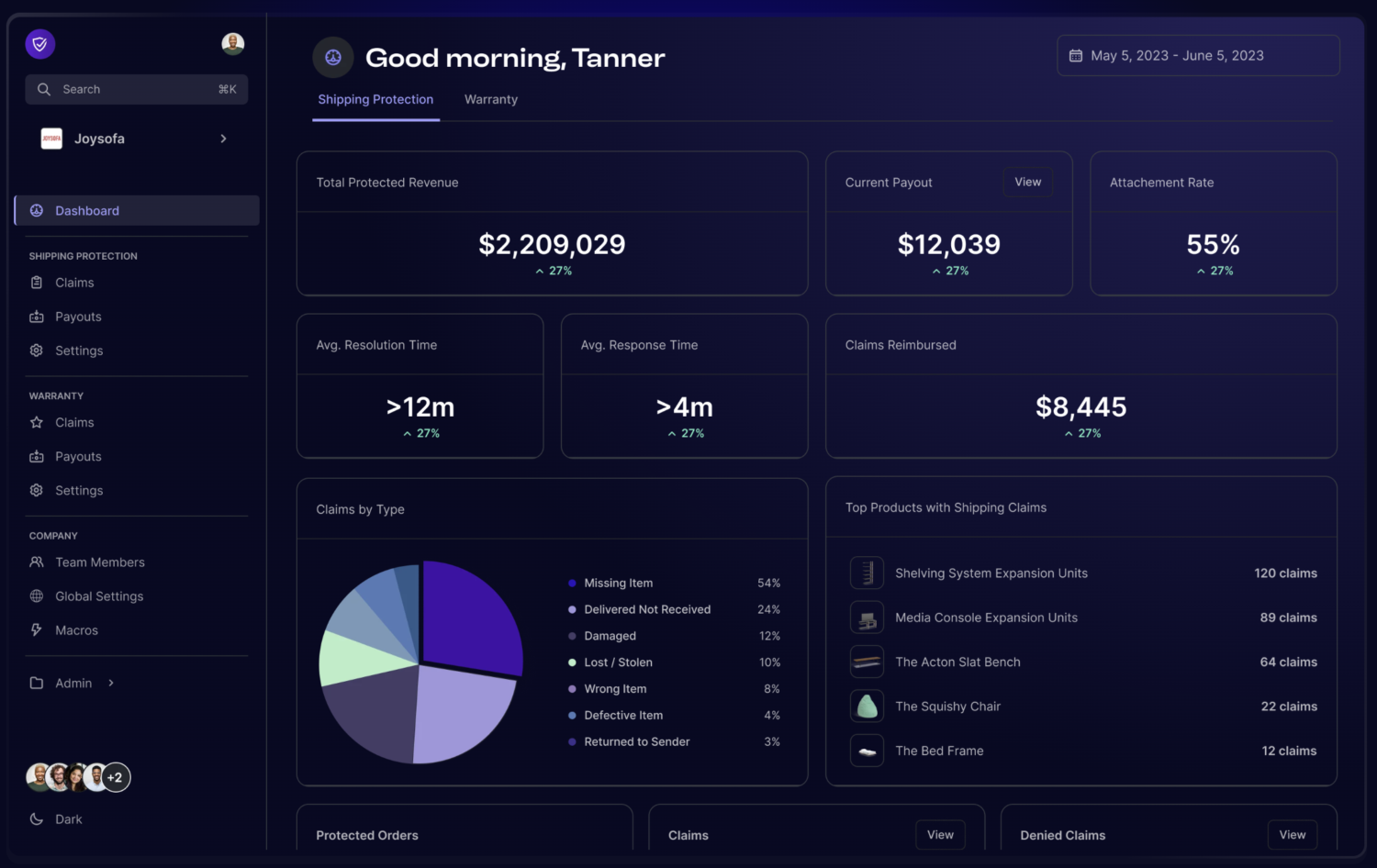

- Judge the pair, never one number. Fraud rate and approval rate move together. A system can post a spotless fraud number by declining everything ambiguous, which quietly costs more than the fraud did. Ask every vendor for both numbers from comparable merchants, and hold your own program to the pair as well.

- Ask how decisions actually get made. Machine learning models catch patterns at scale; expert human review resolves the ambiguous orders that models score in the middle. Systems that combine both tend to protect approval rates better than pure automation, because the gray zone is precisely where false declines are manufactured. Ask what happens to an order the model cannot confidently score.

- Demand explainability. When an order is declined, your team should be able to see why, challenge it, and correct it. Black-box declines are unauditable, untrainable, and corrosive to the customer relationship. Decision transparency is also what lets you fix the model when it is wrong.

- Test on your data before you commit. A backtest against your historical orders, or a parallel pilot on live traffic, tells you more than any reference call. Vendors confident in their accuracy will agree to measurable trials with defined success criteria: approval rate, fraud rate, review rate, and decision latency.

- Probe signal depth. Accuracy comes from evidence. Device intelligence, behavioral signals, network patterns across merchants, and history that connects a returning customer to their own past orders. The question that separates platforms is whether they read intent (what is this buyer here to do?) or only identity (does this card match this address?). Identity checks pass professional fraudsters and fail real customers with new addresses. For more on that distinction, see what customer intentionality means in ecommerce.

Criterion 2: Customer Experience vs Security Is the Wrong Tradeoff

The customer experience vs security framing assumes a dial: turn up protection, add friction, lose some good customers. That is true of blunt instruments and rules stacks. It is not true of accurate decisioning, which is precisely why this criterion belongs in vendor evaluation.

What to look for:

- False decline discipline. Ask vendors how they measure false declines, what their merchants’ rates look like, and what the remediation path is when a good customer gets blocked. A vendor with no false decline story has been optimizing the wrong number.

- Friction that is proportionate, not blanket. Step-up verification has a place on genuinely risky orders. Applied to everyone, it is a conversion tax. The software should reserve friction for the few, invisibly approve the many, and let trusted repeat customers feel recognized.

- A recovery path for wrongly declined customers. The difference between “your order was declined” and a review path that rescues the sale within minutes is measured in lifetime value. Systems with human review convert would-be declines into approvals instead of apologies.

- Support-channel awareness. Customer experience is not only checkout. When your support agents can see risk context (is this refund request the customer’s first, or their fifth this quarter?), they resolve risky moments without punishing honest ones. Fraud decisions that never reach the CX team create the friction merchants notice last.

Good online retail security should be invisible to the customers who fund the business. If a vendor’s answer to fraud is making everyone prove themselves, keep looking.

Criterion 3: Post-Purchase and Journey-Wide Protection

Given where losses moved, this criterion now separates category leaders from legacy point solutions. Evaluate whether the platform can:

- Score refund requests, claims, and returns, not just transactions. Item-not-received claims, empty-box returns, and wardrobing follow patterns the transaction score never sees.

- Connect repeat actors across identities. Serial abusers rotate emails, addresses, and payment methods. Device and behavioral fingerprints connect them. Ask vendors to demonstrate how three “different” accounts sharing a shipping address surface in their system.

- Handle the chargeback lifecycle. Dispute deflection, evidence compilation, and representment belong in the same intelligence loop as screening, because dispute outcomes are training data. Our guide to chargeback prevention in ecommerce covers what that layer should look like in detail.

- Detect bots, resellers, and promo abuse. Account farming and drop-day automation are inventory and margin problems that fraud tooling should see, because the same actors show up later as payment risk.

- Share one customer view across surfaces. The pattern spotted at checkout should inform the return decision. If each surface has its own vendor and none of them talk, the abuser exploits the seams.

Subscription Fraud Prevention: What Changes for Recurring Revenue

Subscription brands carry risks that transaction-scoring tools were not designed around, and the evaluation should reflect them.

The core issue is first order economics. Acquisition discounts, free trial offers, and introductory bundles concentrate value in the first transaction, which attracts abuse that never intends to reach the second bill: prepaid card patterns that leave nothing to charge at rebill, disposable identity patterns that farm new customer offers repeatedly, and promo stacking across alias accounts. The loss shows up not as a chargeback but as a subscriber who evaporates, quietly distorting CAC and cohort math along the way. Our deep dive on prepaid card fraud in subscription programs walks through the mechanics.

For subscription fraud prevention, add these to the evaluation:

- Payment-instrument intelligence at signup, including BIN-level awareness of prepaid and virtual cards, weighed as one signal among many rather than a blunt block.

- Multi-account linking that connects alias signups to one actor before the third free trial, not after the tenth.

- Rebill and involuntary-churn awareness, since fraud controls that ignore the recurring lifecycle miss where subscription revenue actually leaks.

- Friendly fraud readiness on renewals, because “I forgot to cancel” disputes are a structural subscription pattern that evidence and clear cancellation paths reduce together.

The Questions to Ask Every Ecommerce Fraud Prevention Software Vendor

Bring this list to the demo and ask for specifics, not philosophy:

- What approval rate and fraud rate do merchants like us run on your platform, and can you show both?

- What happens to an order your model cannot confidently score? Who reviews it, and how fast?

- How do you measure false declines, and what is the recovery path for a wrongly declined customer?

- Can we run a backtest or parallel pilot on our own traffic with agreed success metrics?

- What do you protect beyond the transaction: returns, claims, promo abuse, chargebacks?

- How do you link one abuser across multiple accounts, addresses, and payment methods?

- Do you offer financial protection on approved orders, and what exactly does it include?

- What does integration require for our stack, and what is the real time to first decision?

- How do our support agents see and use risk context in their tools?

- How does pricing behave at 3x our volume, and during peaks like BFCM or product drops?

Treat vague answers as data. A vendor who cannot show the approval-rate half of the accuracy pair, or whose scope ends at checkout, is telling you where their product ends.

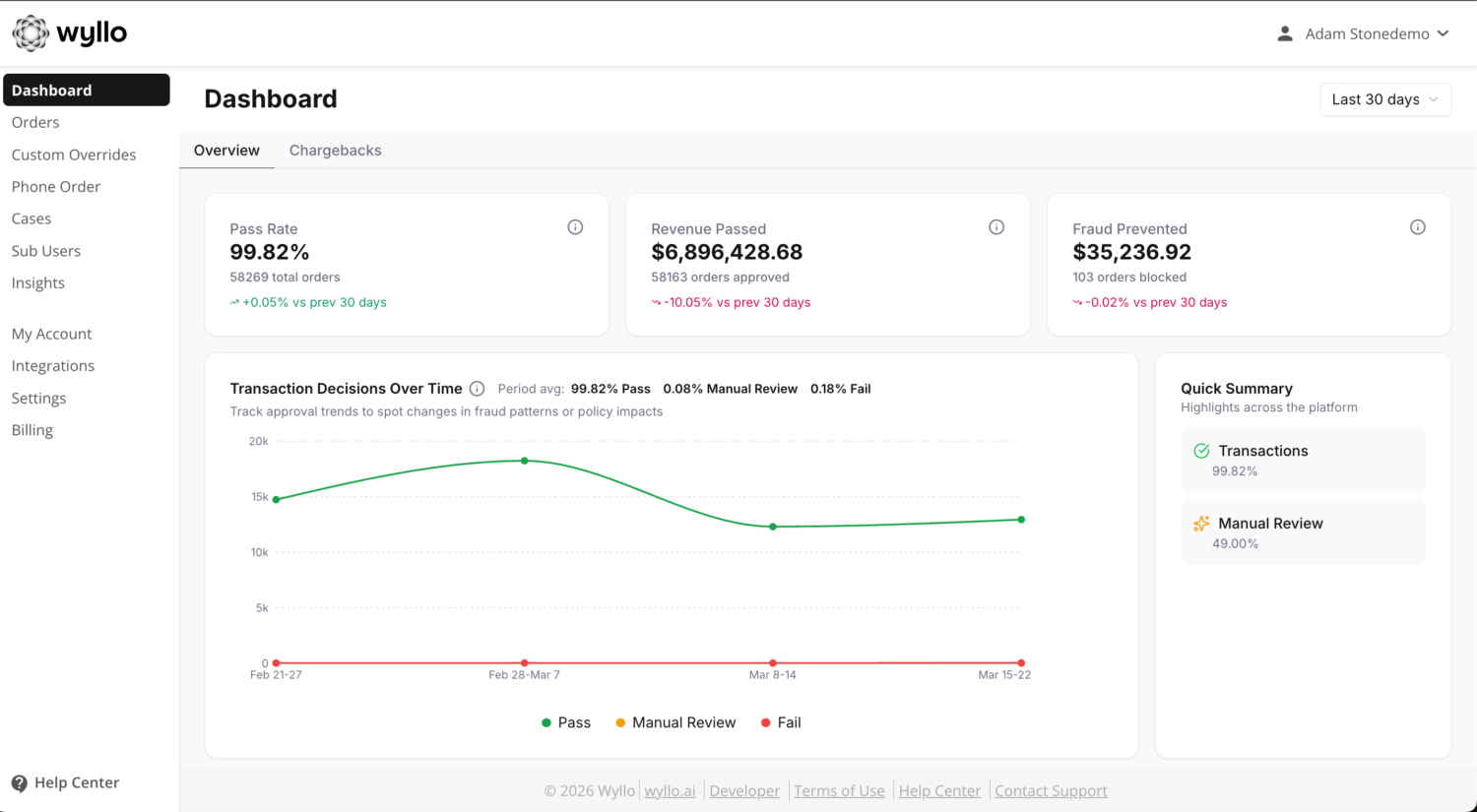

How Wyllo Ecommerce Fraud Prevention Software Helps

The evaluation framework above reflects how Wyllo, the risk intelligence platform for commerce, is built: intent-aware decisioning across the full customer journey, so the signal that stops abuse at checkout also informs the return, the claim, and the dispute.

- Wyllo Payment Fraud Protection combines AI with expert human review to maximize approval rates while stopping payment fraud, with financial protection on approved orders.

- Wyllo Bot and Reseller Detection catches automation, fake account creation, promo exploitation, and unauthorized resellers before they distort inventory and margin.

- Wyllo Return Fraud and Abuse Prevention risk-scores returns and refund claims so serial abuse stops and honest customers keep their easy returns.

- Wyllo Claim and Policy Abuse Prevention catches friendly fraud and policy exploitation in the post-purchase window, before it becomes a chargeback.

- Wyllo Chargeback Management handles dispute responses and representment end to end, with chargeback protection for eligible orders.

- Wyllo CX Support puts risk scores and next-best actions inside the tools your support team already uses.

Judgment over rules.

Frequently Asked Questions

What is ecommerce fraud protection software?

Ecommerce fraud protection software evaluates transactions, accounts, and post-purchase activity to stop fraud and abuse while approving legitimate customers. Modern platforms combine machine learning, device and behavioral intelligence, and in the strongest cases human review to make order-level decisions, and extend protection beyond checkout to returns, claims, promo abuse, and chargebacks.

How do I evaluate fraud detection accuracy before buying?

Ask for the pair of numbers, approval rate and fraud rate, from merchants comparable to you; one without the other is meaningless. Then test on your own data: a backtest against historical orders or a parallel pilot on live traffic with agreed success metrics (approval rate, fraud rate, review rate, decision speed). Vendors confident in their accuracy will agree to measurable trials.

What is the difference between fraud prevention and fraud management software?

Fraud prevention tools focus on stopping bad activity before it completes: screening orders, blocking bots, catching abusive claims. Fraud management software covers the wider operational loop, including case review, chargeback response, reporting, and analytics. In practice the strongest platforms do both, because dispute outcomes and review decisions are the training data that makes prevention smarter.

Do fraud prevention tools hurt customer experience?

Blunt ones do; accurate ones protect it. Rules-heavy systems create false declines and blanket friction that push good customers away. Accurate decisioning approves trusted customers invisibly, reserves verification for genuinely risky orders, and routes ambiguous cases to review instead of auto-declining them. When evaluating vendors, ask specifically how they measure false declines and what happens to a wrongly declined customer.

What should subscription brands look for in fraud protection?

Signals tuned to first order economics: prepaid card awareness at signup, multi-account linking that catches serial free trial and new customer offer abuse, protection through the rebill lifecycle, and evidence readiness for “forgot to cancel” disputes. Transaction-only scoring misses most of these patterns because the loss often arrives without a chargeback, as a subscriber who was never real.

How long does fraud protection software take to implement?

It varies by platform and stack, from days for hosted-checkout integrations with prebuilt plugins to weeks for custom API deployments. The better question is time to trustworthy decisions: ask vendors how long until the system runs at full accuracy on your traffic and what data they need to get there. Verify integration claims against your specific platform before signing.

Bringing It Together

Choosing ecommerce fraud protection software in 2026 comes down to four tests. Can the vendor prove accuracy on your traffic, in both directions? Does the system protect the customer experience rather than tax it? Does its protection extend to where losses now actually occur, after the purchase? And will it scale with the business you are becoming rather than the one you are today?

The category is moving from transaction scoring toward journey-wide risk intelligence, and the gap between those two postures keeps widening as abuse migrates post-purchase. Merchants who buy for the journey now save themselves a second migration later.

Curious how intent-aware decisioning performs on your traffic, on approval rate and fraud rate together? Start with Wyllo Payment Fraud Protection for the transaction layer, or explore the broader Wyllo platform for connected intelligence across the full customer journey.