A practical operating playbook for teams balancing security and customer experience in ecommerce fraud prevention who refuse to choose between stopping abuse and keeping good customers, with current friction data and the metrics that prove you got the balance right

Most fraud programs are described as a dial. Turn security up and you catch more bad actors but add friction that costs you good ones. Turn it down and checkout feels effortless right up until the losses arrive. Framed that way, balancing security and customer experience sounds like a compromise where somebody always loses.

The premise is wrong. Balancing security and customer experience is not about finding the least-bad setting on a single slider. It is about replacing the slider with decisions precise enough that trusted customers move through untouched while genuine risk gets the scrutiny it warrants. The tension only exists when the underlying tool is too blunt to tell the two apart. The stakes for getting this right keep climbing: Juniper Research projects ecommerce fraud losses rising from $56 billion in 2025 to $131 billion by 2030, and every over-correction on the security side hands revenue, and the customer attached to it, to a competitor.

This guide lays out why the tradeoff is a symptom rather than a law, where blunt controls quietly tax the customers you most want to keep, the operating playbook that lets you tighten on abuse without punishing everyone, and how to measure whether you actually struck the balance.

The Tradeoff Is a Symptom, Not a Law

The security-versus-experience conflict is real, but it is a property of the tooling, not of fraud prevention itself. Rules stacks and static thresholds treat every order through the same lens: a rule that blocks risky behavior cannot distinguish a first-time buyer on a new device from a fraudster on a new device, so it either flags both or neither. Tighten the rule and you sweep up the good customer along with the bad. That is the dial everyone complains about.

Accurate decisioning breaks the dial because it judges each order on its own evidence rather than on a blanket condition. The question shifts from “does this order trip a rule?” to “what is this buyer here to do?” A returning customer with a consistent history, a recognizable device, and a normal basket does not need the same treatment as an order that pairs a disposable identity with a mismatched shipping address and a card being tested for the first time. When the system reads intent instead of matching identity alone, protecting the business and protecting the customer stop being opposing goals.

Why Blanket Rules Tax the Customers You Want

The hidden cost of over-tightening rarely shows up as an angry email. It shows up as silence, the good customer who tries once, gets blocked or slowed, and quietly buys elsewhere.

Friction is already the leading reason carts die. Baymard Institute’s checkout research puts the average cart abandonment rate near 70%, with unexpected costs, forced account creation, and a long or complicated checkout among the top reasons shoppers walk. Every security step you add for everyone, an extra verification, a manual hold, a step-up challenge, lands on that same pile. It is felt most by the shoppers a blanket rule was never meant to catch.

False declines are the sharpest version of the same problem. A false decline is a legitimate order wrongly blocked as fraud, and the cost is double: the lost sale now, and the lost lifetime value of a customer who concludes you do not trust them. Legacy rules-based systems are the main manufacturers of these declines, precisely because they cannot separate unusual-but-real from actually risky. The reputational stakes compound the math. Edelman’s 2025 Trust Barometer found 71% of consumers now treat brand trust as a buy-or-boycott factor. Treating good customers as suspects is not a neutral safety measure. It is a slow leak in the top line.

The Operating Playbook for Balancing Security and Customer Experience

Balancing the two comes down to six operating choices. None of them is “accept more fraud.” Each replaces a blunt control with a more precise one.

Decide Upstream, Before the Order Exists

Screen risk at the gateway or before the order is created, not after it lands in fulfillment. Upstream decisioning means suspicious activity is stopped before it becomes an order your team has to unwind, while trusted shoppers complete checkout without ever knowing screening happened. The customer experience benefit is invisibility, and operations spends less time cleaning up after a spike.

Tier Friction to Risk and Trust, Not by Blanket Rule

Reserve verification for the orders that earn it. Lighter treatment for shoppers with clean history and recognizable signals; step-up checks only where the evidence genuinely warrants them. Applied to everyone, step-up verification is a conversion tax. Applied to the few, it is a targeted safeguard the majority never feels.

Read Intent, Not Just Identity

Identity checks answer whether a card matches an address. They pass professional fraudsters who have the right stolen details and fail real customers who moved or bought a gift for someone else. Reading customer intent, the behavioral, device, and relationship signals that reveal what a buyer is actually there to do, is what lets you approve the unusual-but-real order and decline the ordinary-looking-but-fraudulent one.

Keep a Human in the Gray Zone

Pure automation over-declines the ambiguous middle, the high-value first-time buyer, the foreign card, the order that does not fit the model’s idea of normal. Pure manual review does not scale. Pair AI-driven decisioning with expert human review on the gray-zone orders, so an ambiguous case becomes an approval after a second look instead of an automatic loss.

Extend the View Past Checkout

The most damaging abuse now lives after the sale. The Merchant Risk Council’s Global eCommerce Payments and Fraud Report ranks refund and policy abuse as the top fraud threat, ahead of payment fraud, and Mastercard reports first-party (friendly) fraud driving more than 45% of chargebacks. A checkout-only wall does nothing here, and worse, it tempts teams to tighten returns and refunds for everyone to compensate, punishing honest customers for the abusers. Connect signal across returns, claims, support, and disputes so abuse is caught where it happens without blanket policy cuts.

Give Support the Risk Context

Customer experience is not only checkout. When a support agent can see whether a refund request is a customer’s first or their fifth this quarter, they can resolve the risky moment without treating every request as a threat. Risk context inside the tools your CX team already uses turns fraud decisions into better service instead of blanket suspicion.

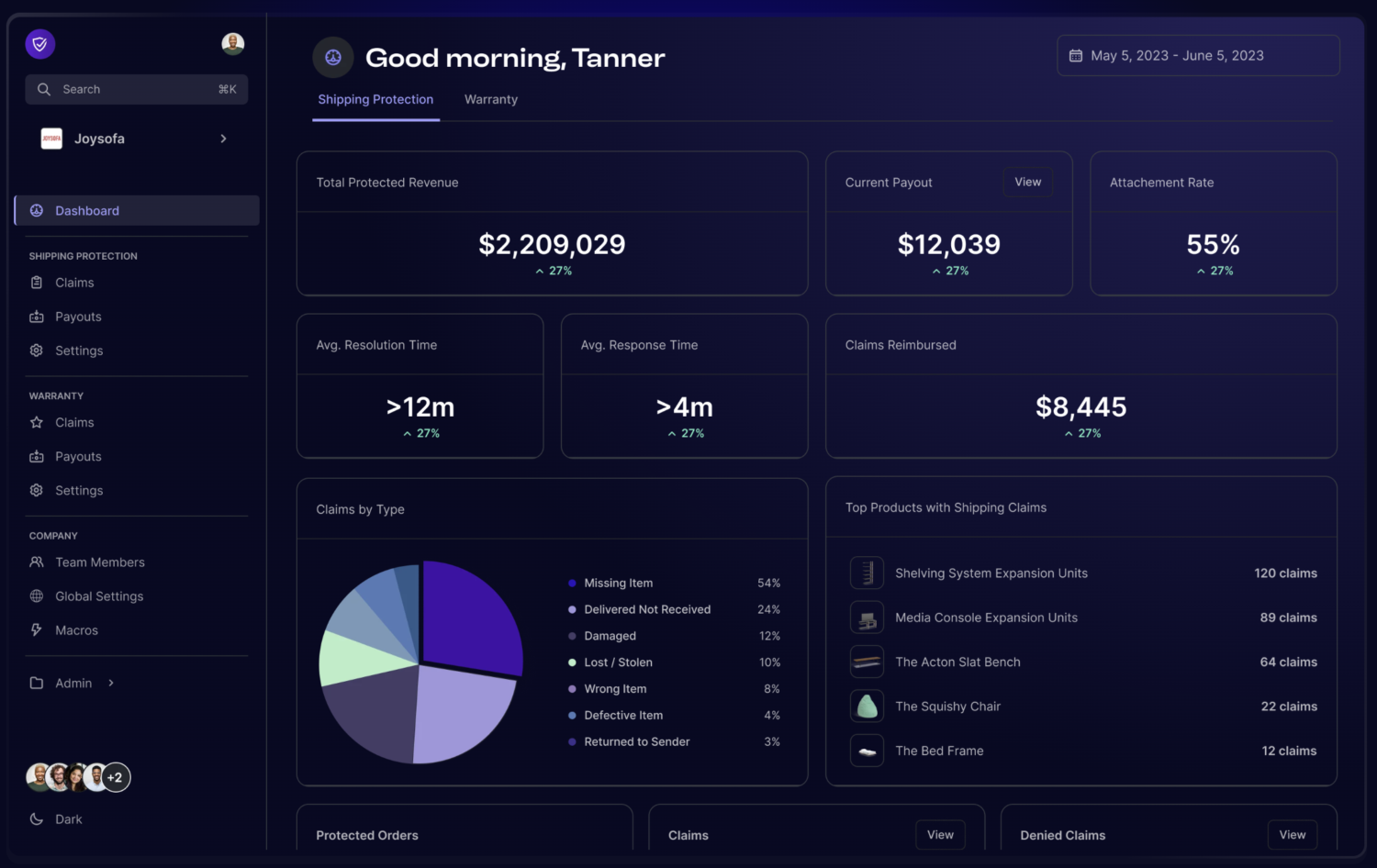

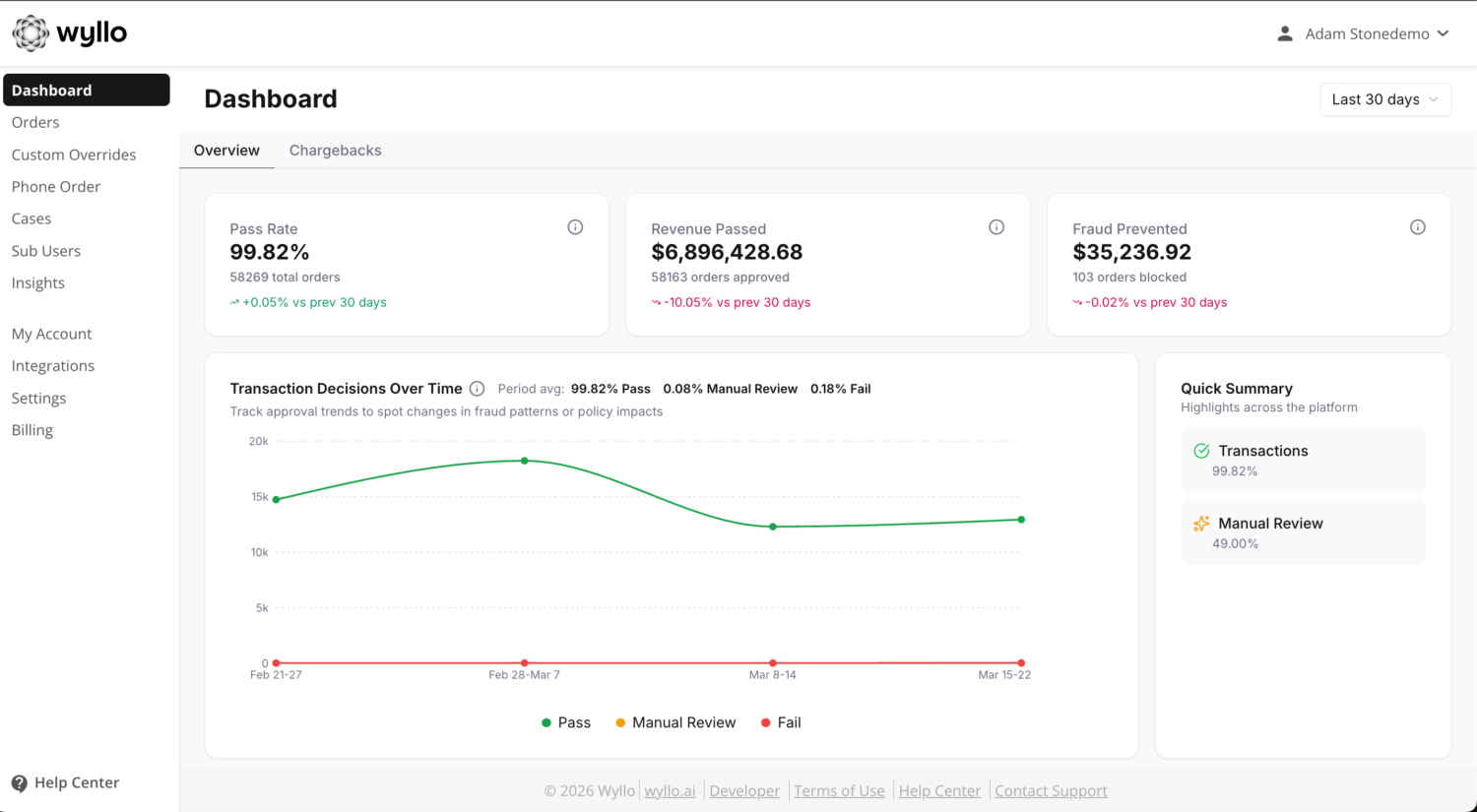

Measure the Balance

You cannot manage a balance you do not measure, and the single most common mistake is watching only the security half. Track these together:

- Approval rate and fraud rate as a pair. Either number alone is a vanity metric. A pristine fraud rate produced by declining everything ambiguous costs more than the fraud it prevented. Judge them together and hold the tradeoff visible.

- False decline rate. If you do not know yours, that is the first finding. Most teams underestimate it badly. It is the clearest measure of how much good business your security posture is quietly rejecting.

- Review rate and decision latency. How many orders need human eyes, and how fast do decisions land? A balance that depends on slow manual queues is not stable at peak.

- Repeat-purchase and first-order approval on new customers. New customer offers and first orders are where over-blocking does the most long-term damage, because a blocked first purchase rarely comes back to retry.

Run these on a quarterly cadence, not just after a fraud spike. The spike is exactly when teams over-tighten, and the review is what pulls the dial back to center.

How Wyllo Helps

Wyllo is the risk intelligence platform for commerce, built on the premise this guide argues: security and customer experience are the same problem solved well, not competing priorities. Intent-aware decisioning is what lets the balance hold.

- Wyllo Payment Fraud Protection pairs AI-driven decisioning with expert human review on the gray-zone orders, lifting approval rates on real customers while stopping payment fraud, with financial protection on eligible approved orders.

- Wyllo Return Fraud and Abuse Prevention risk-scores returns and refunds so serial abuse stops while honest customers keep their easy returns.

- Wyllo Claim and Policy Abuse Prevention catches friendly fraud and policy exploitation in the post-purchase window, before it becomes a chargeback.

- Wyllo CX Support puts risk context and next-best actions inside the tools your support team already uses.

Balancing security and customer experience requires precision over paranoia.

Frequently Asked Questions

How do you balance security and customer experience in fraud prevention?

Stop treating it as one dial. Replace blanket rules with decisioning precise enough to tell a trusted customer from a genuine threat: decide upstream before the order exists, tier friction to risk and trust rather than applying it to everyone, read buyer intent instead of identity alone, keep human review on ambiguous orders, extend protection past checkout, and give support risk context. Then measure approval rate and false decline rate together so the balance stays visible.

Does stronger fraud protection always hurt customer experience?

Only with blunt tools. Rules-heavy systems create false declines and blanket friction because they cannot separate unusual-but-real orders from risky ones, so tightening security sweeps up good customers too. Accurate, intent-aware decisioning approves trusted shoppers invisibly and reserves verification for the orders that warrant it, which improves both numbers at once.

What is a false decline and why does it matter to this balance?

A false decline is a legitimate order wrongly blocked as fraud. It is the clearest sign the balance has tipped too far toward security, and it is expensive twice over: the lost sale, plus the lifetime value of a customer who feels distrusted and shops elsewhere. Tracking your false decline rate is the fastest way to see whether your defenses are rejecting good business.

Which metrics show whether the balance is right?

Approval rate and fraud rate viewed as a pair, false decline rate, review rate and decision latency, and first-order approval on new customers. Watching only the fraud rate hides the cost of over-blocking. Reviewing all of them quarterly, especially right after a fraud spike, keeps the program from over-tightening.

Why isn’t checkout-only fraud protection enough?

Because the fastest-growing abuse happens after the purchase. Refund and policy abuse now ranks as the top fraud threat, and friendly fraud drives a large share of chargebacks. A checkout-only tool misses all of it and pushes teams to tighten returns and refunds for everyone to compensate, which punishes honest customers. Journey-wide signal catches abuse where it happens without blanket policy cuts.

Bringing It Together

Security and customer experience only compete when the tooling forces a choice. The teams that stop treating fraud prevention as a dial, and start treating it as a decisioning problem, get to keep both: abuse blocked where it lives, and trusted customers moving through without a second thought. The levers are practical, decide upstream, tier friction to risk, read intent, keep humans in the gray zone, watch the whole journey, and prove it with approval rate and false decline rate side by side.

The industry is moving from transaction-level rules toward journey-wide risk intelligence, and the gap between the two widens every quarter as abuse migrates past checkout. Merchants who build for that balance now avoid both the fraud losses and the quieter, costlier bleed of good customers turned away.

Curious how intent-aware decisioning would change your approval rate and false decline rate together? Start with Wyllo Payment Fraud Protection, see the full framework in our guide to choosing ecommerce fraud protection software, or explore the broader Wyllo platform for connected intelligence across the full customer journey.