Two of the most common post-purchase losses get used interchangeably, but they happen in different places, through different channels, and call for different defenses. Here’s how to tell friendly fraud vs returns fraud apart.

Friendly fraud and returns fraud are easy to confuse. Both happen after a clean, paid order. Both involve a customer getting their money back on something they arguably shouldn’t. Both are often committed by real people using real identities rather than obvious criminals. But they travel through different channels, the bank versus the merchant, and that distinction changes everything about how you detect and fight them.

This guide to friendly fraud vs returns fraud defines each, lays out where they overlap and where they diverge, and explains how to defend against both.

What Is Friendly Fraud?

Friendly fraud, also called first-party fraud, is when a customer disputes a legitimate charge with their bank instead of resolving it with the merchant. The result is a chargeback. Sometimes it’s deliberate (a shopper who received the goods but wants the money back too); sometimes it’s honest confusion (an unrecognized statement descriptor, a forgotten subscription, a refund that felt slow). Either way, the merchant loses the sale, often the goods, and pays a chargeback fee on top. Mastercard has reported that first-party fraud accounts for a substantial and rising share of all chargebacks.

What Is Returns Fraud?

Returns fraud is the abuse of a merchant’s return and refund process to obtain money or goods dishonestly, through the merchant’s own channel rather than the bank. It includes wardrobing (using an item then returning it as new), empty-box and switch returns, returning stolen goods, and serial refund abuse. The shopper interacts with the merchant’s returns flow, not their card issuer.

The Key Difference in Friendly Fraud vs Returns Fraud: Which Channel

The cleanest way to tell them apart is to ask where the refund came from.

- Friendly fraud goes through the bank. The customer files a dispute with their card issuer, the merchant gets a chargeback, and the contest plays out through the card networks’ representment process, with fees and thresholds attached.

- Returns fraud goes through the merchant. The customer uses the returns and refund process directly, and the merchant pays out from its own systems without a card-network dispute.

That difference drives the defense. Friendly fraud is fought with clear billing descriptors, easy support, and strong representment evidence to win chargebacks. Returns fraud is fought with risk-scored returns, inspection, and policy right-sized to the shopper.

Where They Overlap

The two blur at the edges. A shopper denied a refund through returns may escalate to a bank dispute, turning a returns issue into friendly fraud. A serial abuser may run both channels. And both are frequently committed by genuine customers, which is why neither responds well to blunt “block the bad guys” tactics. The unifying factor is intent: in both cases, the question isn’t only “did this happen?” but “is this a customer acting in good faith or a pattern being worked?”

How to Fight Both

For friendly fraud: make charges recognizable (clear descriptors, proactive billing communication), make support and self-service easy so disputes come to you instead of the bank, and use structured representment to win the chargebacks worth contesting.

For returns fraud: score returns with risk signals, confirm contents on higher-risk returns rather than refunding on a scan, and right-size return policy to the shopper.

For both: connect activity across orders, accounts, and channels so the same actor is recognized whether they hit the bank or the returns desk, and read intent rather than judging each event alone.

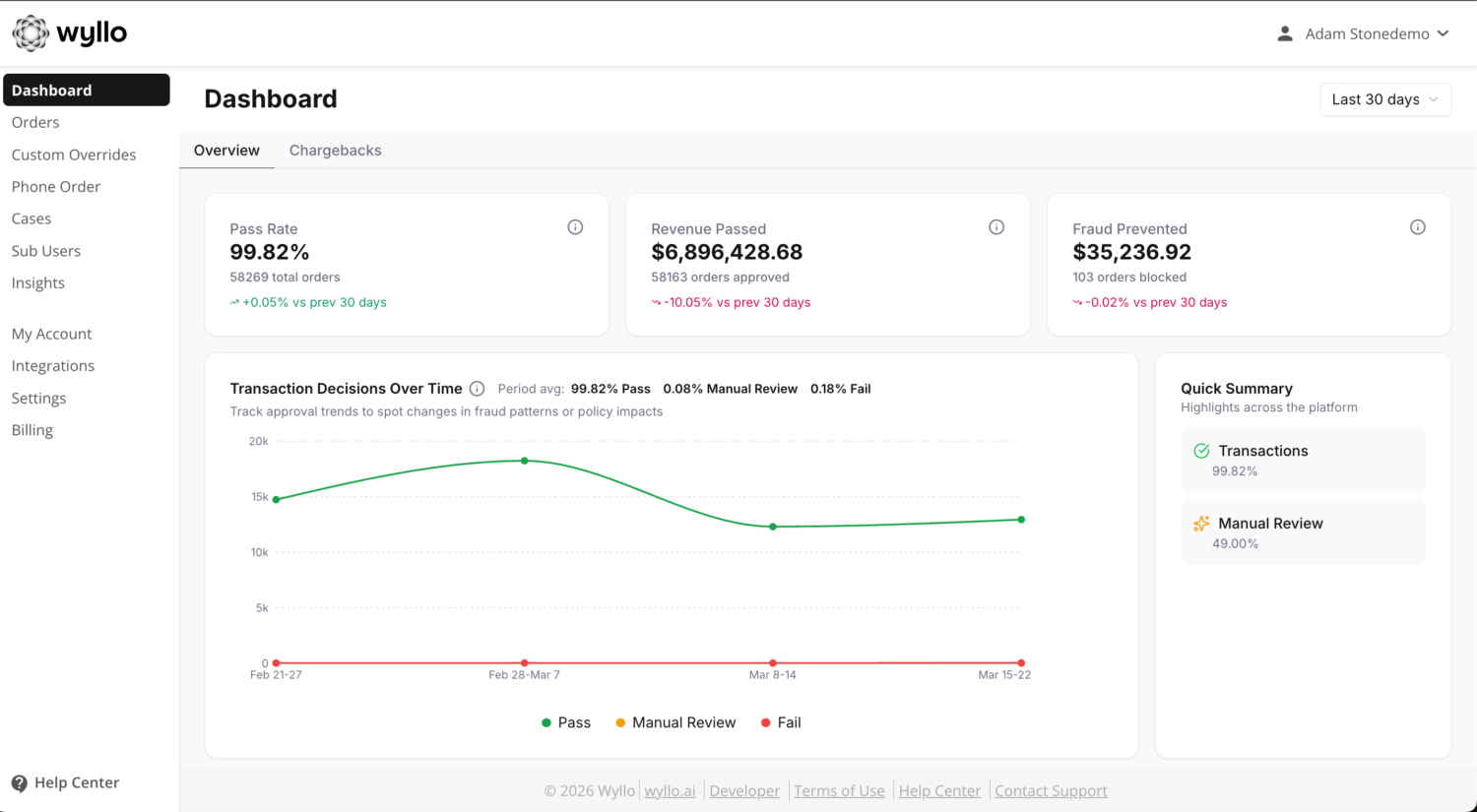

How Wyllo Helps

Wyllo is the risk intelligence platform for commerce, and the connective tissue between these two problems is exactly what it’s built for: the same customer shows up at the returns desk and the dispute line, and only connected signals and intent reveal whether to trust them. Risk surfaces the event; intent explains it.

- Wyllo Chargeback Management handles the friendly-fraud side, turning representment into a structured workflow that recovers more first-party disputes with less manual effort.

- Wyllo Return Fraud and Abuse Prevention handles the returns side, scoring returns and refunds against identity, history, and behavior.

- Wyllo Payment Fraud Protection connects the transaction-level view so the same actor is recognized across channels.

Less reaction. More reason.

Frequently Asked Questions

What’s the difference between friendly fraud and returns fraud?

Friendly fraud is disputing a legitimate charge with the bank, resulting in a chargeback. Returns fraud is abusing the merchant’s own return and refund process. The simplest distinction is the channel: friendly fraud goes through the card issuer, returns fraud goes through the merchant.

Is friendly fraud the same as a chargeback?

Not quite. A chargeback is the mechanism; friendly fraud is one reason a chargeback happens, when a customer disputes a charge that was actually legitimate. Chargebacks can also stem from genuine fraud or real merchant errors.

Can the same customer commit both?

Yes. A shopper denied a refund through returns may escalate to a bank dispute, and serial abusers often work both channels. That’s why connecting activity across orders, accounts, and channels matters: it recognizes the same actor wherever they surface.

How do defenses differ for each?

Friendly fraud is reduced with clear billing descriptors, easy support, and strong representment to win chargebacks. Returns fraud is reduced with risk-scored returns, content verification, and policy right-sized to the shopper. Both benefit from reading intent rather than judging each event in isolation.

Bringing It Together

Friendly fraud and returns fraud look similar from a distance, but the channel they travel through, bank versus merchant, determines how you catch and fight each. What they share is more important than what separates them: both are usually committed by real customers, and both come down to telling good-faith behavior from a worked pattern. That’s a question of intent, read across the whole relationship.

Curious how a connected view would catch the same actor at both the dispute line and the returns desk? Explore the Wyllo platform for connected intelligence across the full customer journey, or start with Wyllo Chargeback Management for the friendly-fraud side.